Getting More Engagement from Employees During Open Enrollment Periods

![Professional couple meeting with their financial advisor. Income Matters.]() There are Few Feelings Worse than Being EXPOSED.

There are Few Feelings Worse than Being EXPOSED.

Before you go deleting your browser history—don’t worry—I’m not talking about anything sinister here.

More along the lines of…

Exposed for doing or saying something hypocritical.

Exposed for not doing the right thing.

Exposed for bad planning.

But we learn from the pain.

And if you’re in the insurance and financial planning profession, it is your responsibility—nay, calling!— to highlight and elucidate these feelings of exposure so your clients fully comprehend what is at stake.

Essentialism and Exposure

Many clients think of “essential insurance” as home and auto.

Losing your uninsured car or home in an unforeseen event would certainly debase most everyone’s financial situation.

That’s why we insure it. It’s valuable coverage.

And it’s (usually) a great risk for insurers:

Property insurance is the simplest transfer of risk—a quantifiable risk based of an asset with a verifiable market; pre-established potential claim value of under $1 million (in most instances).

Contrast that to death or disability.

The value of your earning potential in your 30s, 40s, and maybe even 50s or 60s is much much higher than $1 million.

Much higher.

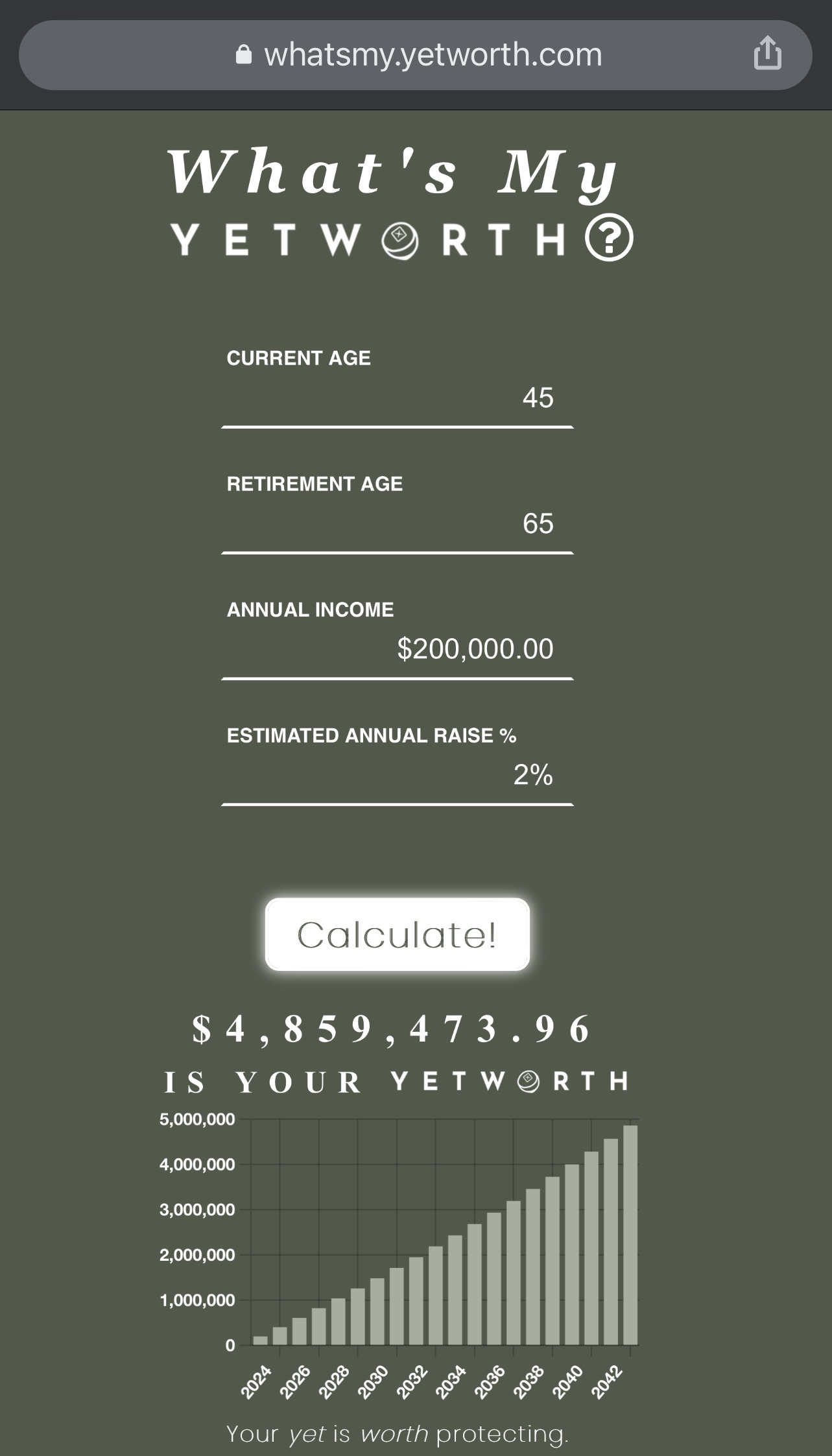

Calculate Earning Potential

Earning potential—or Yetworth, as I like to call it—is simple to calculate.

Take your client’s desired retirement age (65).

Subtract your client’s age. (45)

This is the remainder of their earning years. (20 years)

Then take their annual earnings ($200,000).

And multiply by their remaining earning years (20).

Feel free to add annual increases (2%).

That projects out to $4.86 million!

What’s at Stake

More pointedly, your clients’ family, lifestyle, and financial goals depend on that earning potential.

A premature death or illness could debase all their plans.

There are very few insurances that cover this much exposure for the everyday client.

The Basics vs DEbasics

To your clients life and disability coverage might not feel like “the basics” but they are “debasics” worth insuring.

So pass on the travel insurance, the iPhone coverage, or whatever kitschy “protection plan” is being thrown at you (dare I say pet insurance).

We only advocate for insuring what would debase your financial situation.

Forget the basics. Insure the DEbasics.

Related posts