Getting More Engagement from Employees During Open Enrollment Periods

Our focus was on controlling the costs of our workers’ compensation program. Our WC costs weren’t as high as those of employers in the manufacturing or other manual-labor sectors, because we worked in an office-based industry. Still, the expenses were significant enough to watch closely — and people worried that increased use of office technology and tech-driven job stress might start to ramp up costs. And, besides, we were also a workers’ comp insurer, and actively provided loss-control services to our clients. This meant we needed to show them we managed our own WC exposure as diligently as we were prodding them to manage theirs.

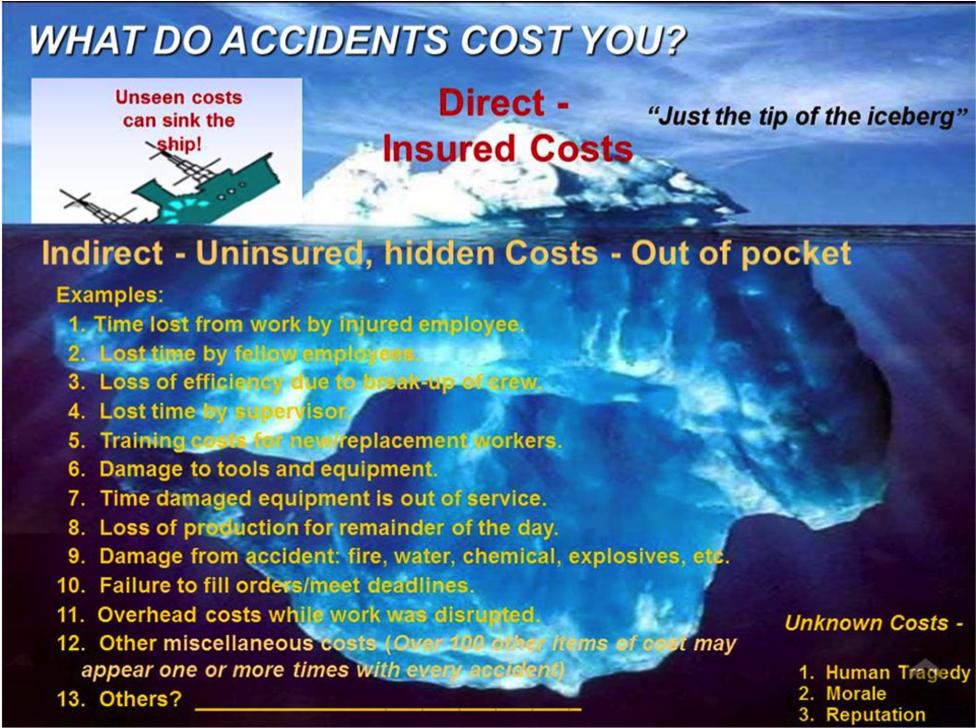

Direct Disability Costs are the Tip of the Iceberg

One of my responsibilities was to do awareness training around safety and loss-control issues for line managers throughout the organization. My manager was big on communicating the bottom-line business value of workplace safety programs. So, we spent a lot of time pointing out how the direct costs of workplace accidents or illnesses were just the tip of the iceberg. The real impact of a WC case was the business disruption that followed in its wake.

As this illustration from a slide deck developed by the U.S. Occupational Safety and Health Administration (OSHA) puts it: “Unseen costs can sink the ship!”

Indirect Non-Occupational Disability Claim Costs

When I took a job with a disability insurance carrier about a decade later, I realized I could apply the iceberg analogy to non-occupational disability, too. The “below the waterline” costs we focused on in WC risk management are just as important— and maybe even more so — when it comes to understanding the impact on short-term disability. The fact is non-occupational disabilities are a lot more common than the occupational disabilities covered under workers’ compensation insurance.

To show you what I mean, let’s look at incidence rates, that is, the number of claims divided by a defined number of people (usually 100 employees).

Comparing WC and STD Claim Incidence Rates

The go-to resource for occupational disability data is the U.S. Department of Labor’s Bureau of Labor Statistics. Every year, they produce a report on workplace illness and injuries based on employer data submitted to OSHA. One of the measures they track is “cases with days away from work” per 100 full time workers— a good surrogate for WC lost-time incidence rate. According to the most recent report (reflecting 2015 data), that rate is 1.0 case/claim per 100 workers across all employment sectors.

On the non-occupational side, there isn’t a data source with the same breadth and depth as BLS. But, the benchmarking database maintained by the Integrated Benefits Institute is a decent alternative. Among other metrics, IBI tracks claims incidence per 100 covered employees for short-term disability programs that, in most cases, cover only non-occupational disabilities due to illnesses, injuries, accidents, or pregnancies.

The most recent database (reflecting 2015 claims activity) contains incidence-rate calculations for over 13,000 employers. The overall average is 5.6 claims per 100 employees. That’s a lot higher than the average 1.0 claim per 100 rate for occupational disabilities.

IBI also provides percentile distributions— just like you see for things like test scores or annual household income. When you look at those, you can see the “sweet spot” found in the 25th to 75th percentile range runs from 2.3 to 7.1 claims per 100 employees. That, too, is higher than the occupational-disability incidence rate of 1.0 per 100.

The Impact of Non-Occupational Disability on Business Operations

So, if the “unseen costs that can sink the ship” are a motivator for your risk management team to address the costs of occupational disabilities, they should be even more of a motivator for your benefits team to address the cost of non-occupational disabilities.

In my September blog post, I’ll share some research-based insights that can help you estimate just how big of an iceberg your company might need to address.

Related posts