Joint Replacements, a Baby Boomer’s Story

This is a crucially important question for us at The Council for Disability Awareness. We would like to see all working Americans have some form of private disability coverage to protect their income when they’re out of work for an extended period of time because of a disabling injury or health condition.

Many people assume they have a safety net with either Workers’ Compensation (WC) or Social Security Disability Insurance (SSDI). But disabling illnesses or injuries are much more likely to be non-occupational in origin, which would rule out coverage under WC. And workers who become disabled off-the-job won’t always qualify for SSDI; they can face average wait times of 600 days for a hearing; and if they do eventually get benefits, the monthly amount (averaging around $1,200, based on the most recent data) probably isn’t enough to help them keep up with their ongoing expenses.

Private disability coverage helps fill the gaps in the safety net. But how many working Americans actually have this important form of income protection?

The answer requires a lot of math — and some assumptions.

It’s important to point out that this number is not readily available. This is due to a number of complex factors, one of which is that disability insurance has traditionally been offered through different channels: as an employee benefit, as a benefit through an association, or on an individual basis. The data therefore is siloed. At The CDA, we’ve gathered data from several industry and governmental sources and have worked with this data through a set of clarifying assumptions — you’ll see these unfold in my argument below.

So, just how large is this problem?

Let’s start by understanding the three ways you can get private disability coverage: through an employer (and there are various ways this can occur, as we’ll explain below); through an association or affinity group; or on an individual basis.

1. Through an employer

This can be in two main ways:

- Coverage is part of a benefits plan and the employer pays some or all of the cost

- An employee voluntarily elects coverage and pays for the entire cost — this includes both cafeteria-style benefits and worksite enrollment plans

a) Employer pays all or some:

The Bureau of Labor Statistics (BLS) Employee Benefits Survey is the go-to source for data on number of working Americans covered by employer-provided disability insurance (where the employer pays for all or at least part of the cost of coverage). Unpublished BLS estimates from the most recent (March 2017) National Compensation Survey show 49.4 percent of all civilian workers as having some form of employer-paid disability insurance (short-term disability only, long-term disability only, or both STD and LTD).

If we apply this percentage to 139.9 million, which is the latest (2017) BLS estimate of civilian workers in the U.S. (excluding Federal Government employees, who are not included in the Employee Benefits Survey), we get approximately 69.1 million working Americans in this, the biggest category of working Americans with some form of private disability coverage.

But that leaves 70.8 million who either are covered in some other way or aren’t covered at all. And that’s why we next look at the alternate way people can get coverage through their employer.

b) Employee pays all (voluntary coverage)

A growing number of employers are offering disability coverage on a voluntary basis. Employees can sign up for disability coverage, and they pay the full cost, but usually at attractive group rates and with the advantage of payroll deduction for premiums. Because they pick up the tab for premiums, if they do wind up collecting benefits at some point, they’ll receive those benefits on a tax-free basis. (On the other hand, benefits are taxable under a disability plan where the employer has paid the premium.)

How many of the roughly 70.8 million working Americans not covered under employer-paid disability insurance are protected by some form of voluntary coverage? There are two keys needed to unlock the answer.

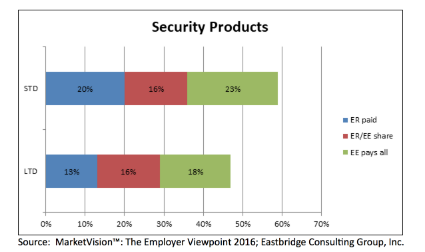

The first is to get an estimate of how many employers offer disability insurance as a voluntary benefit. I asked Ginger Bates, research director at Eastbridge Consulting Group, a widely respected consultancy specializing in the voluntary space. Bates shared the following highlight from Eastbridge’s latest MarketVision Employer Viewpoint survey:

The graph shows, with respect to short-term disability (STD) and long-term-disability (LTD) coverage, the percentage of employers reporting they offered it on a fully employer-paid basis (blue), shared-payment basis (red), or employee-paid basis (green). It also shows, indirectly (if you subtract the total of blue + red + green from 100 percent), the percentage of employers that don’t offer the coverage at all.

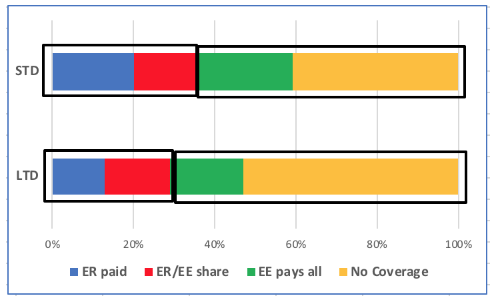

We can redraw the graph to include “no coverage” as a fourth option:

Here, we’ve drawn a box around the blue plus the red. That box corresponds to the scope of the BLS survey (remember, they’re only looking at coverage paid in whole or in part by the employer). And we’ve drawn another box around the green plus the yellow. That corresponds to what’s outside the scope of the BLS survey. Within that second box, the green (percentage of employers who offer disability coverage, but the employee has to pay the entire cost) accounts for about a third of that box.

Now, let’s get back to our 70.8 million (the estimated number of working Americans who don’t have employer-paid disability insurance). It’s not unreasonable to assume that a third of them could be eligible for voluntary disability coverage offered through their employer.

But remember, this is voluntary coverage. Only those employees who actually sign up for the coverage (and, of course, pay the premiums) can be counted as covered. That’s why getting a handle on what the industry calls the “participation rate” (percentage of eligible employees who actually get the coverage) is so important here.

We turned once more to the experts at Eastbridge. They periodically survey voluntary insurance carriers on participation rates by coverage and provide that information to their subscribers. Eastbridge research director Ginger Bates provided findings from their most recent (year-end 2017) survey:

- Short-term disability: 29 percent

- Long-term disability: 34 percent

Given the greater percentage of employers offering STD coverage (based on other Eastbridge research, and also consistent with what BLS has found with respect to employer-paid coverage), let’s use an overall participation rate of 30 percent — which also happens to be consistent with what I observed when I worked at two different carriers.

The way we estimate how many people are covered by voluntary (employee pays all) coverage is:

Number of workers without employer-paid coverage (70.8 million)

X

Percent where employer offers voluntary coverage (33%)

X

Participation rate (30%)

This works out to just over 7 million.

2. Association/ affinity business

Employer-provided disability insurance (including voluntary) covers the largest number of working Americans. But it’s not the only way workers can get covered on a group basis. Another way is through a plan offered to members of a professional society (for example, the American Institute of Certified Public Accountants) or an affinity group like a college alumni association.

Disability coverage is just a piece of the larger “association/affinity” market, which includes property/casualty coverages such as auto and homeowners as well as a variety of life-insurance offerings.

The Professional Insurance Marketing Association, more commonly known as PiMA, represents most of the insurance carriers that serve this market. In 2013, it conducted a market survey, results of which are highlighted here. Based on the data they share in the public-facing report, we applied a series of assumptions:

PiMA reports that its members account for close to $10 billion in premiums with a total of 26 million certificates (i.e., individuals covered — and yes, one person can have multiple certificates, but in the interests of simplicity we’ll assume certificates = individuals). It also reports that approximately 30 percent of members’ sales involved life and health products (most association/affinity business involves property/casualty products).

Based on those numbers, we can estimate:

- Average premium per certificate = $385 ($10 billion in premium divided by 26 million certificates)

- Estimated total life and health premium = $3 billion (30% of $10 billion total)

- Total life and health certificates = 7.8 million ($3 billion estimated total premium divided by estimated $385 premium per certificate)

It’s unlikely that every life and health certificate will involve disability coverage — but let’s use the 7.8 million as an upper limit to the number of people covered through this channel.

3. Individual disability

Individuals can also purchase a disability policy on their own. This is usually organized through an agent or broker. As is the case with the voluntary and association/affinity markets, there’s no comprehensive, publicly available data that gives an indication of how many people have coverage through this channel.

However, individuals with considerable experience in this facet of the business can make informed, “back of the envelope” calculations that give us a starting point. One of our contacts estimates that approximately six million workers have disability insurance on an individual basis.

Of those six million, we don’t know how many rely only on their individual disability policy for coverage, as opposed to those who have bought an individual policy to supplement coverage they already have either through their employer or an association affinity group to which they belong. For now, let’s assume that individual coverage is all they have.

Putting it all together

- 69.1 million working Americans receive disability insurance as part of their employee benefit plan, and their employer pays some or all of the cost of coverage

- 7 million have chosen to purchase disability insurance through their employer, but are paying the entire cost out of their own pockets

- As many as 7.8 million working Americans belong to some kind of group like a professional organization or alumni society that provides access to disability insurance, and that’s how they purchase coverage

- 6 million have worked with their financial advisors to obtain their own individual disability insurance policy (which may or may not be the only one that provides them coverage)

Assuming there’s no double-counting for any of these categories (and there probably is, but let’s simplify for the sake of argument here), this adds up to as many as 89.9 million working Americans who are covered by some form of disability insurance other than WC or SSDI.

But remember, we’re looking at a base of 139.9 million workers (excluding Federal Government). That would leave up to 50 million uncovered. That’s more than one in three working Americans who are potentially uncovered.

Are you one of them? If you are, do yourself — and those close to you who depend on your income — a favor, and visit our new educational website to learn how disability insurance works.

Join the conversation: As I mentioned earlier, a lot of “clarifying assumptions” have been applied in this article. I welcome a “sanity check” of those assumptions — and the numbers to which they’ve been applied — from readers who have experience in this area. Write to us at info@disabilitycouncil.org

Related posts